The french research credit tax guide

MESR

This guide mentions the articles of the General Tax Code (CGI) and those of the Tax Procedure Book (LPF) to which it refers. However, these references and quotes are used for informational purposes and within the educational goal of this guide. They do not in any way replace the texts themselves and have no legal value. This guide is not binding on the administration

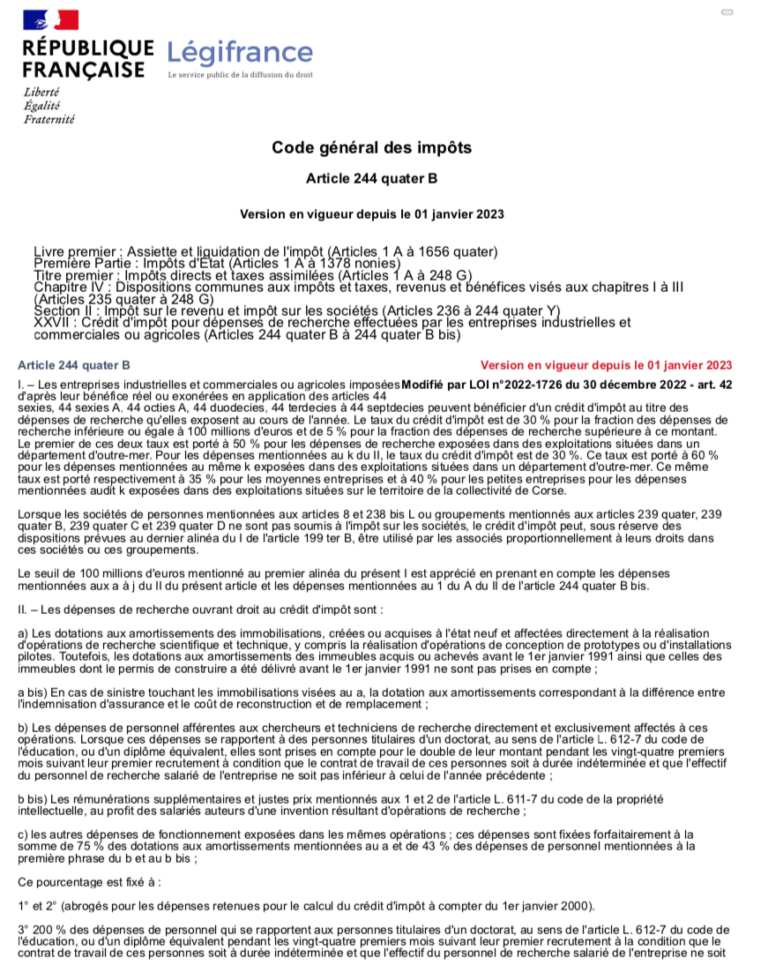

244 quater B Article

Legifrance

Industrial, commercial and agricultural companies subject to income tax can benefit from the CIR under the conditions defined in Article 244 quater B.

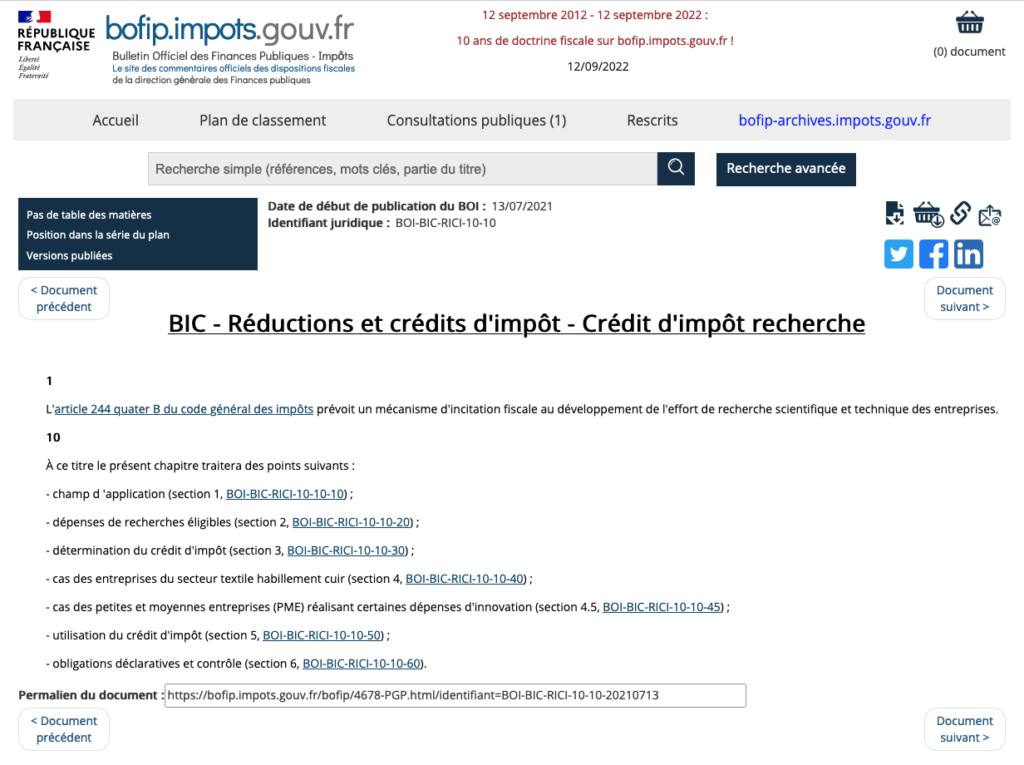

Bulletins officiels des impôts

BOFIP

Article 244 quater B provides a tax incentive mechanism for the development of scientific and technical research efforts by companies, as illustrated in the following law text: