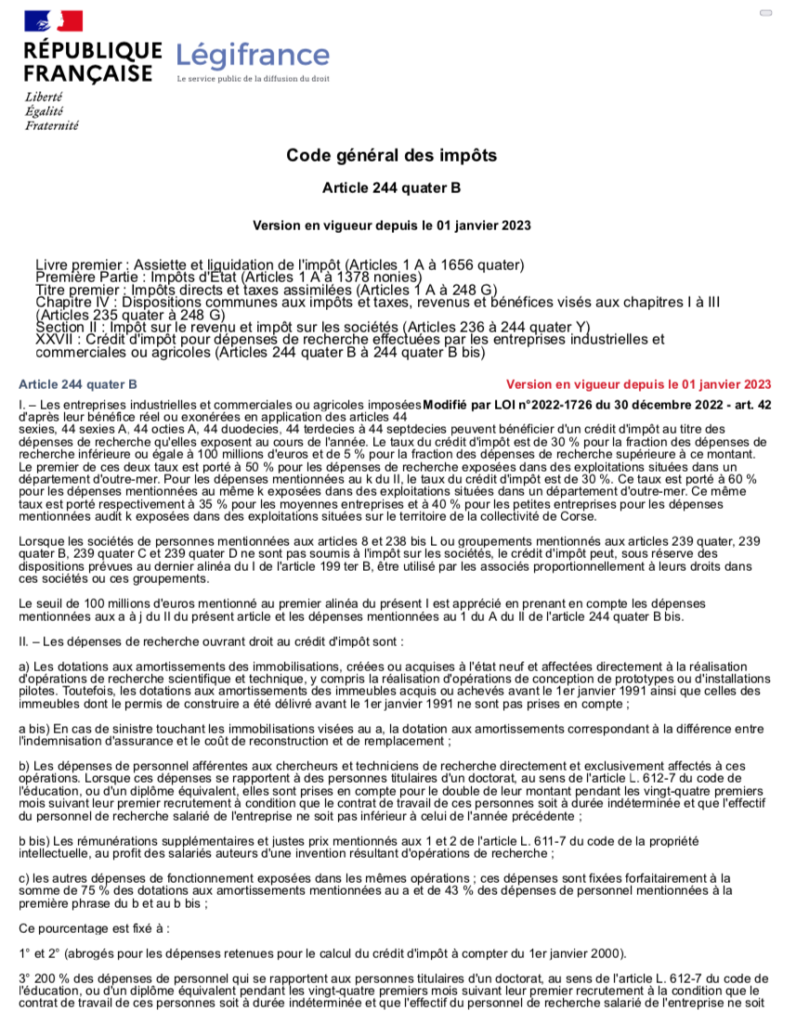

244 quater B Article

Legifrance

Le CII est défini dans k de l'article 244 quater B.

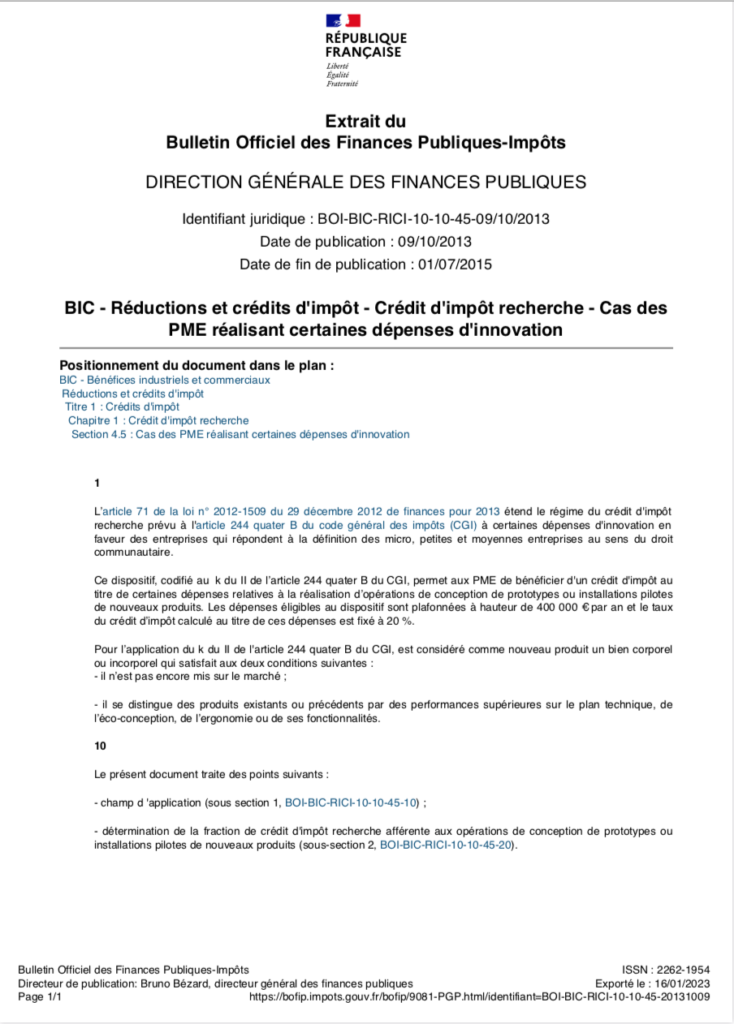

Bulletin Officiel des Impôts

BOFIP

Article 244 quater B provides a tax incentive mechanism for the development of innovative products as shown in the following BOFIPs: